Algeria Healthcare Environment Outlook

Algeria Macroeconomic, Political & Healthcare Environment Outlook

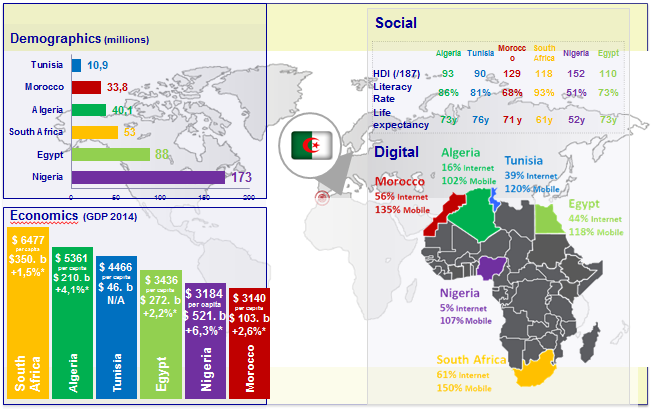

Algeria is the largest pharmaceutical market in Africa

Stable macroeconomic indicators despite an economy largely dependent on oil price variations.

95% of Algeria Foreign Exchange Revenues are generated by Oil and Gaz (30% of GDP). The Oil Barrel price recovered from 30 USD at end 2015, up to 53 USD during the first month of 2017. With a state budget at 50 USD/barrel, Algeria will continue to face economic tensions throughout 2017

Health, education and army remains priority pillars for the government

In 2016, Algeria's growth reached 3.4% (vs 2.8% in 2015), and is expected to continue to grow by 2.8% in 2017.

Growth was driven by the domestic demand, which remained protected by the state’s heavy subsidies on basic necessity goods, high amount of public investments and exports of hydrocarbons.

External trade shows a $17.84Bn deficit in 2016 vs $13.71Bn deficit in 2015, an increase of 4.8%.

Hydrocarbon exports have suffered a reduction of 17.12% vs 2015, which considerably impacted the balance. As a result, imports have also slowed down by 9.62% in order to lessen the impact, but they still represented $46.73Bn vs $61.7Bn in 2015, highlighting the country’s strong dependency on foreign goods.

- In this more volatile economic environment, the Health Budget will remain a priority. Health coverage and Reimbursement are carved in the Algerian Constitution.

- Industrial Investments remain critical to continue to exist, eg Novartis moved from 100 m usd sales in 2014 down to 35 m usd in 2016 due to their absence of Industrial Strategy. MSD, GSK, Pfizer, Abbot followed the same trend.

- 51%/49% Obligation of Algerian equity for all investments made since June 2009.

- Local Manufacturing Obligation in Algeria for pharma companies since 2008.

- Local Manufacturing Obligation in Automotive since 2014.

Key figures of the Pharmaceutical market access

- High Inflation (4,8%/2015), due to Dinar depreciation

- Transfers of dividends not allowed

- Termination of payment through Letters of Credits as from